May’s Top Billers 2026

May's Top Bills 2026

Autumn’s settling in, but the bills aren’t slowing down. We’ve crunched the May numbers and the top four billers are no surprise: tax, rent, rates and school fees are doing the heavy lifting. However you choose to pay, whether via BPAY or BSB & Account Number, Sniip turns those everyday bills into points. Curious where you stack up? Scroll on.

land tax NSW, qld land tax, land tax calculator, land tax victoria, land tax qld, nsw land tax, queensland land tax, sto land tax, land tax calculation nsw, land tax queensland, land tax threshold nsw, victoria land tax, nsw land tax calculator, victorian land tax, qld land tax changes

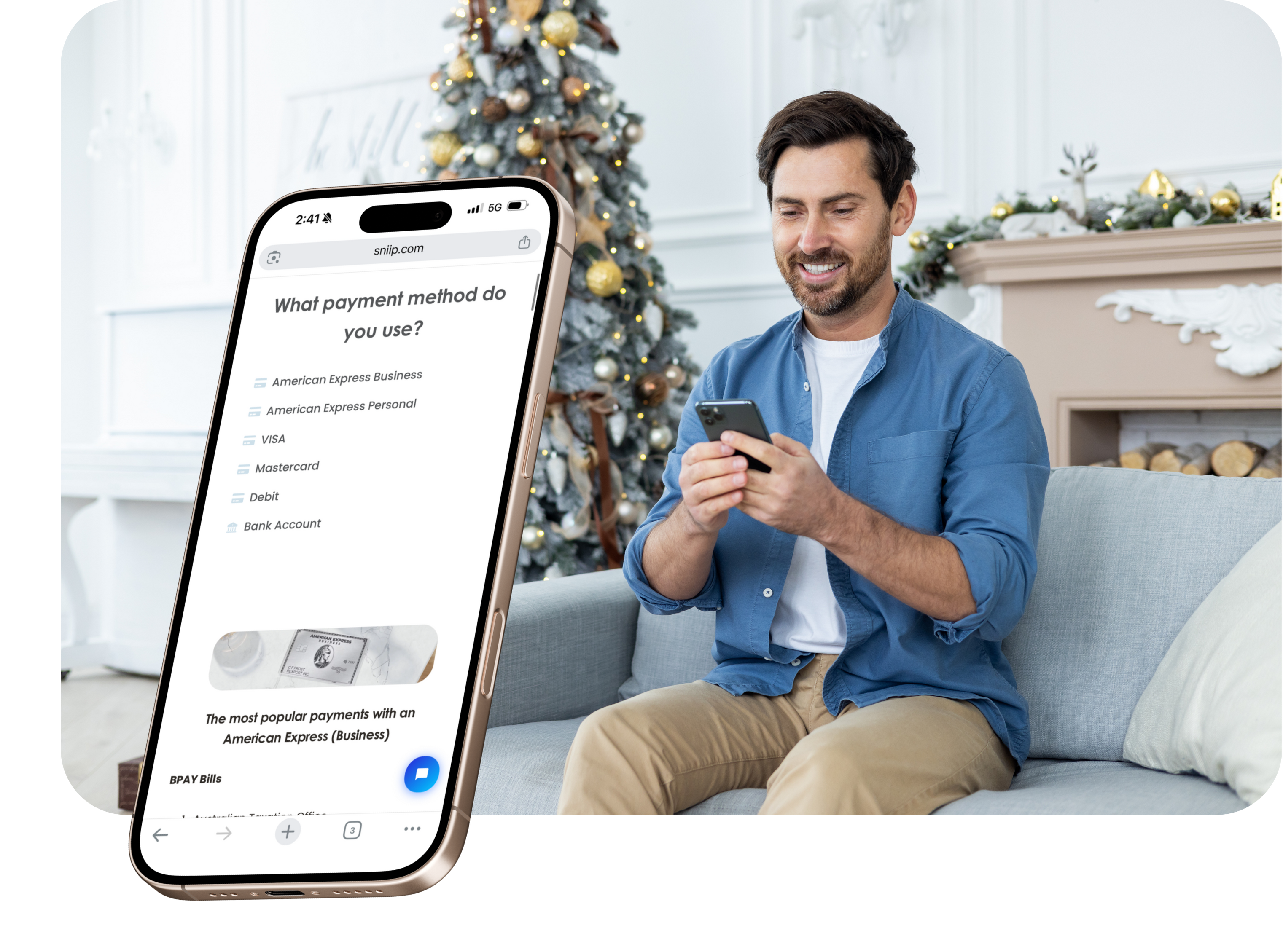

What payment method do you use?

The most popular payments with an American Express (Business)

BPAY Bills

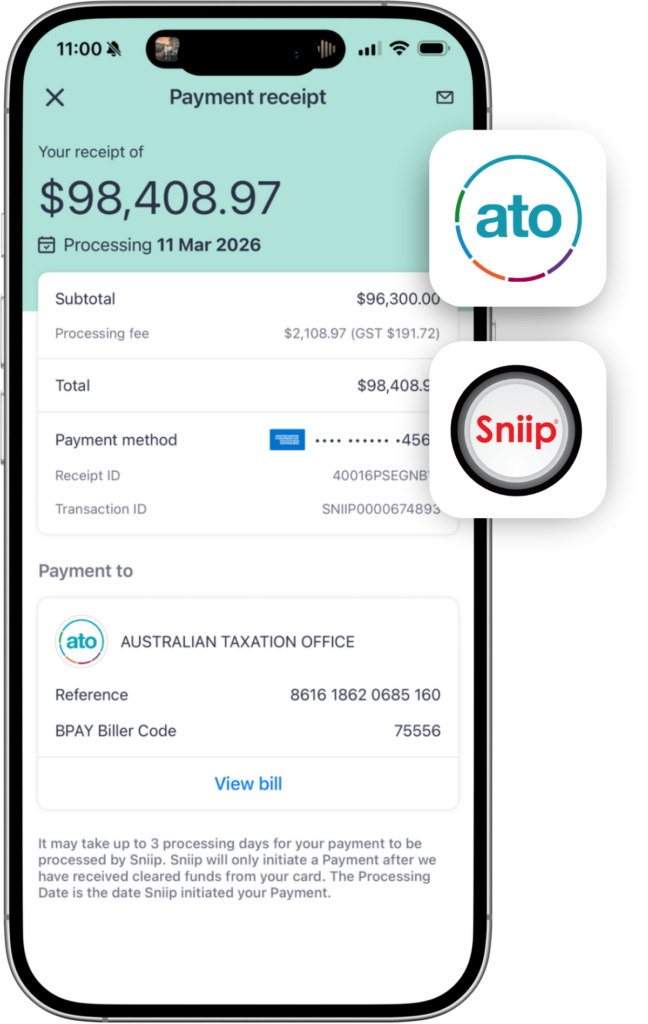

- Australian Taxation Office

- ASIC

- Centrelink

- Child Support Agency

- Rates (e.g. Brisbane City Council, City of Sydney, City of Melbourne, City of Gold Coast, City of Casey, Logan City Council, Knox City Council, Sutherland Shire Council, Monash Council, Cairns Regional Council, Glen Eira City Council, Ipswich City Council, Toowoomba Regional Council, Mornington Peninsula Shire Council, Liverpool City Council)

- Superannuation and Personal Contributions (e.g. UniSuper Member Voluntary Contributions, QSuper Voluntary Contribution, MLC Super Fund, AustralianSuper, Host Plus, Sunsuper Member Voluntary Post Tax Contribution)

- Education (e.g. Trinity Grammar School Kew, Haileybury College, Kingswood College, Our Lady of Mercy College, Brindabella Christian College Lyneham, Our Lady of the Rosary Primary School Kensington, St Peters Primary School Inglewood, Saint Stephens College, Modern Teaching Aids)

- Cleaning & Waste Services (e.g. Cleanaway Operations, AMC Commercial Cleaning)

- Legal Services (e.g. Legal Practitioners Liability Committee)

- Utilities (e.g. AGL Sales, Origin Energy, Alinta Energy Retail Sales, Synergy, EnergyAustralia, Ergon Energy QLD, Globird Energy, Urban Utilities, Sydney Water, Yarra Valley Water Corporation, Icon Water, South East Water, Water Corporation of Western Australia)

Non-BPAY Bills

- Superannuation Funds

- Accounting Services

- Real Estate Services

- Road Freight Transport

- Nursery Production

- Tyre Retailing

- Concreting Services

- Waste Treatment and Disposal Services

- Electrical Services

- Hardware and Building Supplies

The most popular payments with an American Express (Personal)

BPAY Bills

- Australian Taxation Office

- ASIC

- Centrelink

- Child Support Agency

- Rates (e.g. Brisbane City Council, City of Sydney, City of Melbourne, City of Gold Coast, City of Casey, Logan City Council, Knox City Council, Sutherland Shire Council, Monash Council, Cairns Regional Council, Glen Eira City Council, Ipswich City Council, Toowoomba Regional Council, Hornsby Shire Council, Wollongong City Council)

- Revenue / Land Tax (e.g. Revenue NSW, State Revenue Office Vic Land Tax, ACT Revenue Office, Revenue SA Land Tax, Revenue NSW Fine, Revenue NSW Debt, Fines Victoria, Fines Enforcement and Recovery Unit, Brisbane City Council Parking Fine, City of Gold Coast Infringements)

- Storage Services (e.g. Fort Knox Mansfield, National Storage North Melbourne)

- Security Systems (e.g. ADT Security)

- Public Transport (e.g. Public Transport Authority of Western Australia)

- Telecommunications (e.g. Telstra Corporation, Optus Billing Services, Vodafone Postpaid, Aussie Broadband, iiNet, Southern Phone Company, AGL Telco, Leap Telecommunications, Tangerine Telecom, Internode, Flip TV, Superloop, UNITI Internet)

Non-BPAY Bills

- Real Estate Services

- Specialist Medical Services

- Advertising Services

- Structural Steel Fabricating

- Sports and Physical Recreation Clubs and Sports Professionals

- Higher Education

- Clothing Retailing

- Carpentry Services

- Fire and Security Alarm Installation Services

- Taxi and Other Road Transport

The most popular payments with a VISA

BPAY Bills

- Australian Taxation Office

- ASIC

- DEFT Payments (e.g. DEFT Payment Systems, DEFT Real Estate)

- Strata Pay – Unit Levies

- Child Support Agency

- Rates (e.g. Brisbane City Council, City of Sydney, City of Melbourne, City of Casey, Logan City Council, Knox City Council, Sutherland Shire Council, Ipswich City Council, Glen Eira City Council, Hume City Council, Ku-ring-gai Council, Toowoomba Regional Council, Sunshine Coast Regional Council, Mornington Peninsula Shire Council, Northern Beaches Council)

- Workers Compensation (e.g. icare Workers Insurance NSW)

- Real Estate Services (e.g. Nelson Alexander x Kolmeo, Melcorp Real Estate, Xynergy Realty South Yarra, Jam Real Estate Sunbury, Areal Property, Dynamic Residential Group, Meriton Property Services, Cubbi, Montgomery Real Estate, Metropole Property Management, L J Hooker Canberra City, Serengeti Property Management, TWT Realty, Etan Keeter)

- Education (e.g. Ballarat Grammar School, Edstart Australia, Catholic Education Diocese of Wollongong, Catholic Schools Broken Bay, St Bede’s College)

- Health Insurance & Medical (e.g. Bupa, Police Health, Latrobe Health Services, Hospital Contribution Fund of Australia, Medibank Australia)

Non-BPAY Bills

- Real Estate Services

- Residential Building Construction

- Superannuation Funds

- Accounting Services

- Fruit and Vegetable Wholesaling

- Scientific and Technical Services

- Performing Arts Operation

- Child Care Services

- Warehousing and Storage Services

- Education

The most popular payments with a Mastercard

BPAY Bills

- Payway Rent & Hire

- Hair & Beauty (e.g. De Lorenzo Hair Care)

- Australian Taxation Office

- Rates (e.g. Brisbane City Council, City of Sydney, City of Melbourne, City of Gold Coast, City of Casey, Logan City Council, Knox City Council, Sutherland Shire Council, Monash Council, Cumberland Council, Hume City Council, Toowoomba Regional Council, Sunshine Coast Regional Council, Mornington Peninsula Shire Council, Northern Beaches Council)

- Revenue / Land Tax (e.g. Revenue NSW, State Revenue Office Vic Land Tax, ACT Revenue Office, OSR QLD Land Tax, SPER, Fines Victoria Instalment Arrangements)

- Superannuation and Personal Contributions (e.g. AustralianSuper, Host Plus, Retail Employees Superannuation Trust)

- Real Estate Services (e.g. Nelson Alexander x Kolmeo, Meriton Property Services, Frasers Property Management VIC, G and H Property Group, Cimino Real Estate Group, Soames Real Estate)

- Education (e.g. Combined Schools, Catholic Schools Broken Bay, St Christopher’s Primary School Holsworthy, Mary MacKillop College, Catholic Education Diocese of Wollongong)

- Utilities (e.g. AGL Sales, Origin Energy, Alinta Energy Retail Sales, EnergyAustralia, Red Energy, Momentum Energy, GloBird Energy, Energy-On, Supa Energy, Power and Water Corporation, Telstra Limited, Telco Payment, Optus Billing Services, Vodafone Postpaid, iiNet, Southern Phone Company, Leap Telecommunications, Flip TV)

- Centrelink

Non-BPAY Bills

- Real Estate Services

- Adult, Community and Other Education Services

- Non-Residential Property Operators

- Corporate Head Office Management Services

- Accounting Services

- Health Care Services n.e.c.

- Warehousing and Storage Services

- Accounting Services

- Gardening Services

- Legal Services

The most popular payments with a debit card

BPAY Bills

- Australian Taxation Office

- DEFT Payments (e.g. DEFT Payment Systems, DEFT Real Estate)

- Strata Pay – Unit Levies

- Rates (e.g. Brisbane City Council, City of Sydney, City of Melbourne, City of Gold Coast, City of Casey, Logan City Council, Sutherland Shire Council, Toowoomba Regional Council, Sunshine Coast Regional Council, Mornington Peninsula Shire Council, City of Greater Geelong, Wyndham City Council, Townsville City Council, Adelaide Hills Council, Cassowary Coast Regional Council)

- Revenue / Land Tax (e.g. State Revenue Office Vic Land Tax, SPER, Revenue NSW Debt, Fines Victoria Instalment Arrangements, Fines Enforcement Registry, NT Department of the Attorney-General and Justice Fine)

- Real Estate Services (e.g. Nelson Alexander x Kolmeo, Ray White Mildura, The 1888 Co, Residential Rental Agreement)

- Education (e.g. St Aidan’s Primary Rooty Hill, Marist College Bendigo, Suncoast Christian College)

- Health Insurance & Medical (e.g. Medibank Private, Teachers Health Fund, Defence Health, NIB Health Funds, Australian Health Management Group, Hospital Contribution Fund of Australia)

- Direct Debit Services (e.g. QuickPay)

- Utilities (e.g. AGL Sales, Origin Energy, Alinta Energy Retail Sales, Synergy, EnergyAustralia, Ergon Energy QLD, Red Energy, Simply Energy, 1st Energy, CovaU Energy, Jacana Energy, Sumo Vic, Arcline by RACV Energy)

Non-BPAY Bills

- Real Estate Services

- Legal Services

- Health Services

- Parking Services

- Tertiary Education

- Funeral, Crematorium and Cemetery Services

- Sports and Physical Recreation Services

- Construction Services

- Waste Treatment and Disposal Services

- Adult and Community Services

The most popular payments with a bank account

BPAY Bills

- Rates (e.g. Brisbane City Council, City of Gold Coast, City of Casey, City of Parramatta, Logan City Council, Liverpool City Council, Sutherland Shire Council, Monash Council, Hornsby Shire Council, Toowoomba Regional Council, Sunshine Coast Regional Council, Northern Beaches Council, Canterbury-Bankstown Council, Mosman Council, Redland City Council)

- Revenue / Land Tax (e.g. Revenue NSW, SPER, Fines Victoria, Fines Enforcement and Recovery Unit)

- Superannuation and Personal Contributions (e.g. OneSuper Professional Super, AustralianSuper)

- Australian Taxation Office

- ASIC

- DEFT Payments (e.g. DEFT Payment Systems, DEFT Real Estate)

- Strata Pay – Unit Levies

- Credit Cards & Banking (e.g. American Express, ANZ Banking Group Cards, NAB Cardholder Services, Westpac Banking Corporation Card Services, St George Bank Cards, Bank of South Australia Cards, Bank of Melbourne Cards, Bankwest Credit Card, Citibank Credit Cards, Macquarie Card Services, Coles Mastercard, GO Mastercard, Gem Visa Card, Qantas Credit Cards, Police/Nurse Credit Society)

- Security Systems (e.g. ADT Security)

- Real Estate Services (e.g. Jellis Craig Eltham)

Non-BPAY Bills

- Real Estate Services

- Advertisement Services

- Creative Artists, Musicians, Writers and Performers Services

- Technical and Vocational Education and Training

- Electrical Services

- Accounting Services

- Goods and Equipment Rental and Hiring

- Child Care Services

- Plumbing Services

- Health Services